FSCS compliance: The Future of Depositor Protection

HSBC Bank plc (HBEU) and HSBC UK Bank plc (HBUK)’s January 2024 fine, imposed by the Prudential Regulation Authority (PRA) for historic failures in deposit protection identification and notification, alongside the 2023 United States banking crisis underscore the importance of rigorous data governance and quality for FSCS compliance. HSBC’s penalty, the second largest by the PRA, shows the consequences of poor data management, while the 2023 US banking crisis reveals the systemic risks of liquidity concerns and market instability.

These incidents emphasise the need for mechanisms to safeguard financial stability. The Financial Services Compensation Scheme (FSCS), established in the United Kingdom, embodies such a mechanism, created to instil consumer confidence and prevent the domino effect of bank runs.

What is Single Customer View (SCV)?

The FSCS plays a crucial role in uncertain times: if a bank collapses, its compensation mechanism must activate immediately to maintain confidence. The PRA Rulebook (Section 12) requires firms to produce a Single Customer View (SCV)- a detailed record of eligible deposits- within 24 hours of a bank’s failure or upon request.

This quick, accurate response ensures timely compensation, preventing banking crises. With the FSCS now covering up to £85,000 per individual, the 24-hour SCV mandate significantly enhances financial sector security and depositor trust.

What data challenges does SCV pose?

With SCV regulation, the demand for accurate and consistent depositor records presents specific, often challenging, data quality issues. Financial institutions must ensure each depositor’s record is accurate and meets SCV's detailed requirements.

5 data challenges associated with SCV:

-

Identification and rectification of duplicated records– As a result of disparate data entry points or legacy systems.

-

Lack of consistency across records– Customer details may vary across different systems e.g. misspelt names or outdated addresses.

-

Data timeliness– SCV necessitates that data be updated within 24 hours, requiring real-time (or near-real-time) processing capabilities. Legacy systems, often built on batch processing, may struggle to adapt.

-

Discrepancies in account status — Determining if an account is active, dormant, or closed must be resolved to prevent compensation delays/ errors.

-

Aggregating siloed data–SCV mandates involve aggregating data across multiple product lines, account types, and geographies, a task that can be formidable given the legacy data structures and the diversity of regulatory environments.

The HSBC fine underscores the ramifications of inaccurate risk categorisation under the depositor protection rules and the insufficiency of stress testing scenarios tailored to depositor data. Without robust data quality controls, banks risk misclassifying depositor coverage, which can lead to regulatory sanctions and reputational damage.

Integrating SCV with wider data strategies

Effective depositor protection requires more than SCV compliance; it demands a broad approach to data governance and quality, positioning SCV as a critical component of a comprehensive account and customer-level data strategy.

To overcome these challenges, financial institutions must not only deploy advanced data governance and quality tooling but also foster a culture of data stewardship where data quality is an enterprise-wide responsibility, not just IT’s.

By adopting rigorous data standards and validation processes enterprise-wide, banks can turn data management from a regulatory burden into a strategic asset.

An enterprise approach involves:

-

Unified data governance frameworks: Establishing data governance frameworks that ensure data accuracy, consistency, and accessibility across the enterprise.

-

Advanced data quality measures: Implementing measures to keep customer data up-to-date and reliable.

-

Integration with broader business objectives: Aligning SCV and other regulatory data requirements with broader business objectives, including risk management, customer experience enhancement, and operational efficiency.

-

Leveraging technology and analytics: Employing cutting-edge technology to streamline data management processes, from data collection and integration to analysis and reporting.

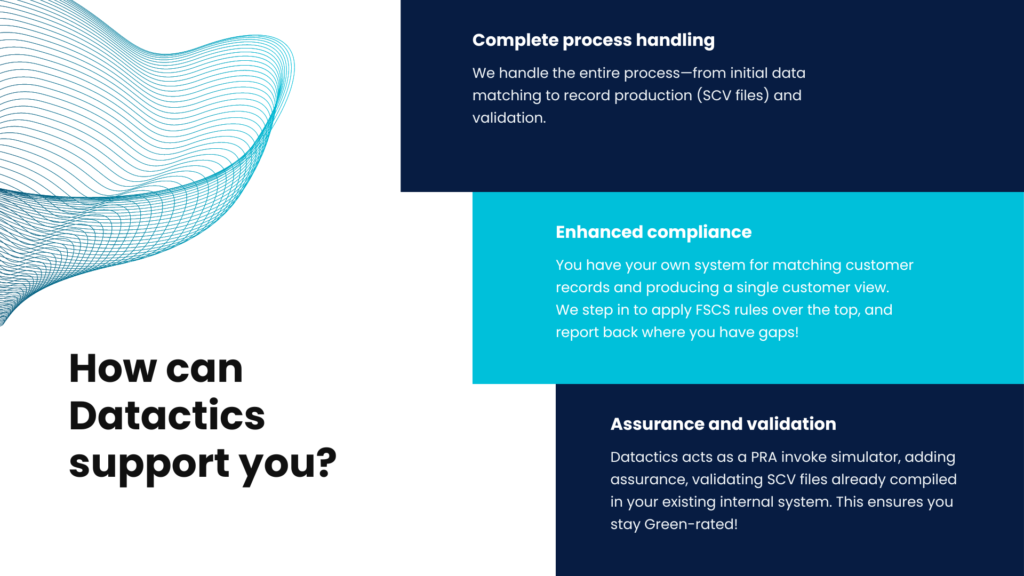

How can Datactics help?

At Datactics, we understand that the challenges posed by regulations like SCV indicate broader issues within data management and governance.

Our approach transcends the piecemeal addressing of regulatory requirements; instead, we advocate for and implement a comprehensive data strategy that integrates SCV within the wider context of account and customer-level data management.

Our solutions are designed to support regulatory compliance but also to bolster the overall data governance and quality framework of financial institutions.

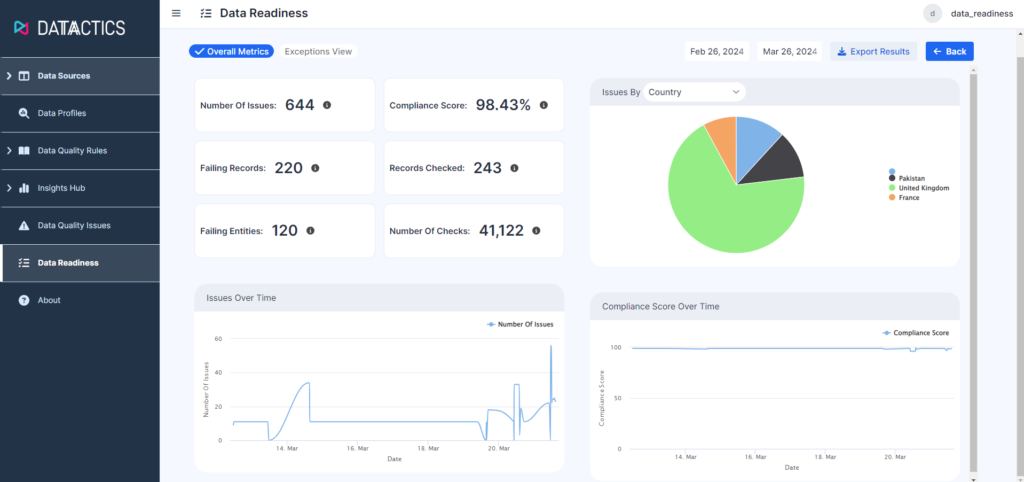

'Datactics' FSCS Data Readiness Solution'

We work closely with our clients to:

-

Identify and address data quality issues through advanced analytics and machine learning.

-

Implement robust data governance practices that align with both regulatory requirements and business goals.

-

Foster a culture of data excellence that values data accuracy, consistency, and transparency.

We support our customers with navigating FSCS compliance, not simply by addressing regulations in isolation, but by integrating them into a broader, strategic framework. By doing so, we ensure compliance and protection for depositors whilst paving the way for a more resilient, trustworthy, and efficient banking sector.

Ella Gago-Brookes

Ella joined techUK in November 2023 as a Markets Team Assistant, supporting the Justice and Emergency Services, Central Government and Financial Services Programmes, before progressing into Junior Programme Manager in January 2024.

Authors